Selling power across state lines in India is not just a commercial decision — it is a multi-layered regulatory exercise. Between connectivity transfer rules, tapering ISTS waivers, surcharge structures, and bidding mandates, a project that looks viable on paper can quickly become uneconomical without careful planning. This note maps the four regulatory dimensions every Independent Power Producer must resolve before signing a term sheet.

Structuring the Asset: SPV and Connectivity Transfer

Connectivity under CERC's General Network Access (GNA) Regulations is granted to a specific legal entity, not to a project site. This makes the corporate structure the first and most consequential decision for any developer acquiring an existing project.

The most bankable route is to acquire the Special Purpose Vehicle (SPV) that holds the connectivity, rather than just the underlying assets. When an entrepreneur takes over an SPV, the technical milestones already recorded — financial closure progress, land acquisition — remain valid under the original connectivity grant, avoiding a full re-application under Form CONN-TRANS-APP-3 with the Central Transmission Utility (CTU).

Land eligibility adds a parallel condition. For solar projects, the lease term must be coterminous with the Power Purchase Agreement — typically 25 years. Regulators require proof of clear title or leasehold rights for at least 50% of the project land to sustain connectivity validity. Gaps here can trigger connectivity suspension at the worst possible moment.

Connectivity transfer to a new developer is a formal regulatory process handled by the CTU under Regulation 15 of the CERC (GNA) Regulations. Allow 60–90 days for this process when structuring acquisition timelines.

ISTS Waivers Are Tapering — The 2027 Window Is Closing

For most of the last decade, the 100% waiver of Inter-State Transmission System (ISTS) charges made long-distance renewable power commercially attractive. That window has now closed. The full waiver expired for projects commissioned after June 30, 2025, under the latest Ministry of Power notifications.

Projects commissioned between July 2026 and June 2027 — the realistic window for a project ready in 12 to 15 months — are eligible for a 50% ISTS charge waiver only. That waiver tapers further to 25% in FY 2027–28 before full charges apply. For developers underwriting long-distance supply agreements today, this is the single most important number in the financial model.

Transmission losses are a separate and permanent cost. For every 100 units generated at the source state, only approximately 96 units are credited at the delivery point in the destination state. Unlike ISTS charges, these losses are almost never waived and must be built into every tariff and PPA negotiation from day one.

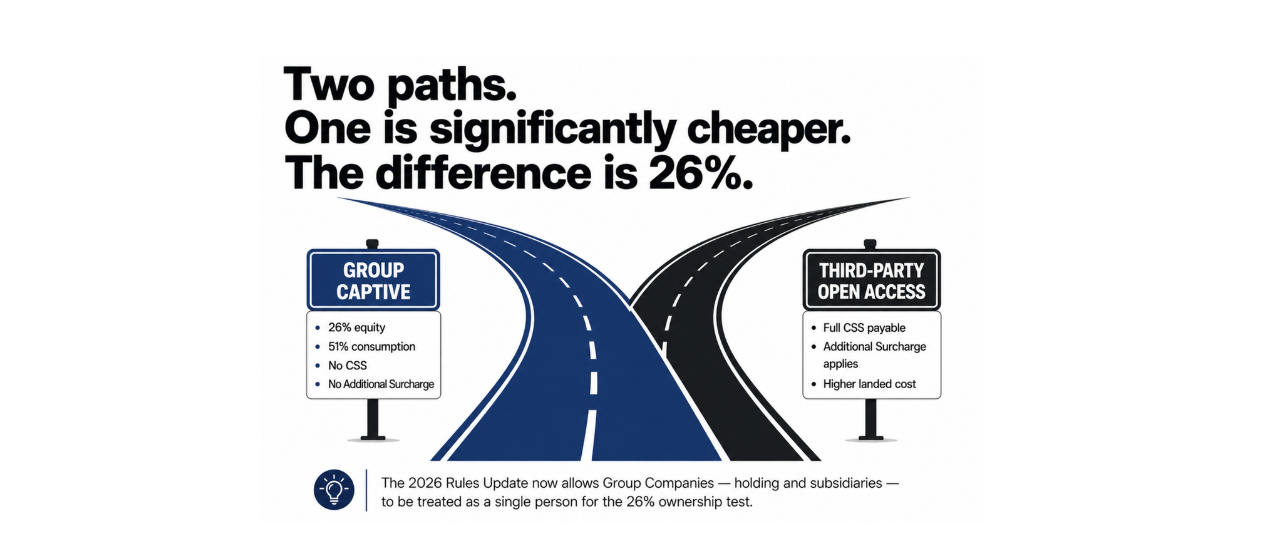

Group Captive vs Third-Party Sale: The Surcharge Decision

When an IPP sells to an industrial user rather than a utility, two distinct regulatory paths exist — and the choice between them can change the landed cost of power by 20% or more.

- Industrial user holds 26% equity in the SPV

- User must consume at least 51% of energy generated

- Fully exempt from Cross-Subsidy Surcharge (CSS) and Additional Surcharge (AS)

- 2026 Rules Update: Group companies (holding + subsidiaries) treated as a single "person" for the 26% ownership test

- No equity requirement on the industrial user

- Full CSS applies — capped at 20% of average cost of supply

- Additional Surcharge also payable on top

- Simpler to structure commercially, but significantly increases the consumer's landed power cost

If the 26% equity threshold is not met or the 51% consumption condition lapses in any year, the transaction is reclassified as Third-Party Open Access — triggering full CSS and Additional Surcharge liability retrospectively. Developers must build monitoring and cure mechanisms into the shareholders' agreement.

Large corporate groups with multiple subsidiaries should use the 2026 Rules amendment — which treats holding and subsidiary companies as a single "person" for the 26% ownership test — to structure Group Captive arrangements across group entities without concentrating equity in a single balance sheet.

Selling to Utilities: The Bidding and Adoption Layer

Entering into a long-term PPA with a distribution utility introduces a different set of procedural requirements. Most state utilities are mandated to procure power only through transparent, competitive bidding under Section 63 of the Electricity Act. A private IPP must win an auction — there is no direct negotiation route for long-term bilateral contracts with state discoms.

The tariff discovered in the bid is not self-executing. It must be formally adopted by the State Electricity Regulatory Commission (SERC) of the buying state before the PPA becomes legally binding. This process exists to protect end consumers and can add 30–60 days to financial closure timelines.

For inter-state supply specifically, the National Load Despatch Centre (NLDC) acts as the nodal verification agency. The NLDC confirms the actual flow of power and ensures compliance with the buying state's Renewable Purchase Obligation (RPO) targets — a condition that can affect PPA tenor and volume commitments.

The Four Cost Layers Every Developer Must Model

Inter-state power supply carries four unavoidable charges: GNA charges (capacity reservation on the national grid), ISTS charges (the transmission toll, now at 50% waiver for 2027 projects), wheeling charges (last-mile distribution network cost at the destination), and RLDC/SLDC operating charges (real-time scheduling fees). A project that ignores any one of these four layers will not survive its first tariff review.

- Acquire the SPV, not just the assets — connectivity rights, land milestones, and technical progress travel with the legal entity, not the site.

- Model the 50% ISTS waiver for 2027 commissionings and stress-test at 25% for 2027–28 delays — the full-charge scenario is no longer hypothetical.

- Structure industrial supply as Group Captive wherever possible; the 2026 Rules amendment makes this viable for large corporate groups without concentrating equity risk.

- Budget 3.5–4% transmission loss as a permanent, unwaived cost in every inter-state PPA model.

- Allow 60–90 days in project timelines for SERC adoption of bid tariffs and CTU connectivity transfer processing.

India's inter-state power market is maturing — and with maturity comes regulatory precision. Developers who treat the GNA framework, ISTS waiver schedule, and surcharge architecture as financial variables rather than legal footnotes will be the ones structuring bankable projects in 2026 and beyond. The rules are complex, but they are knowable — and knowing them is where margin is made.